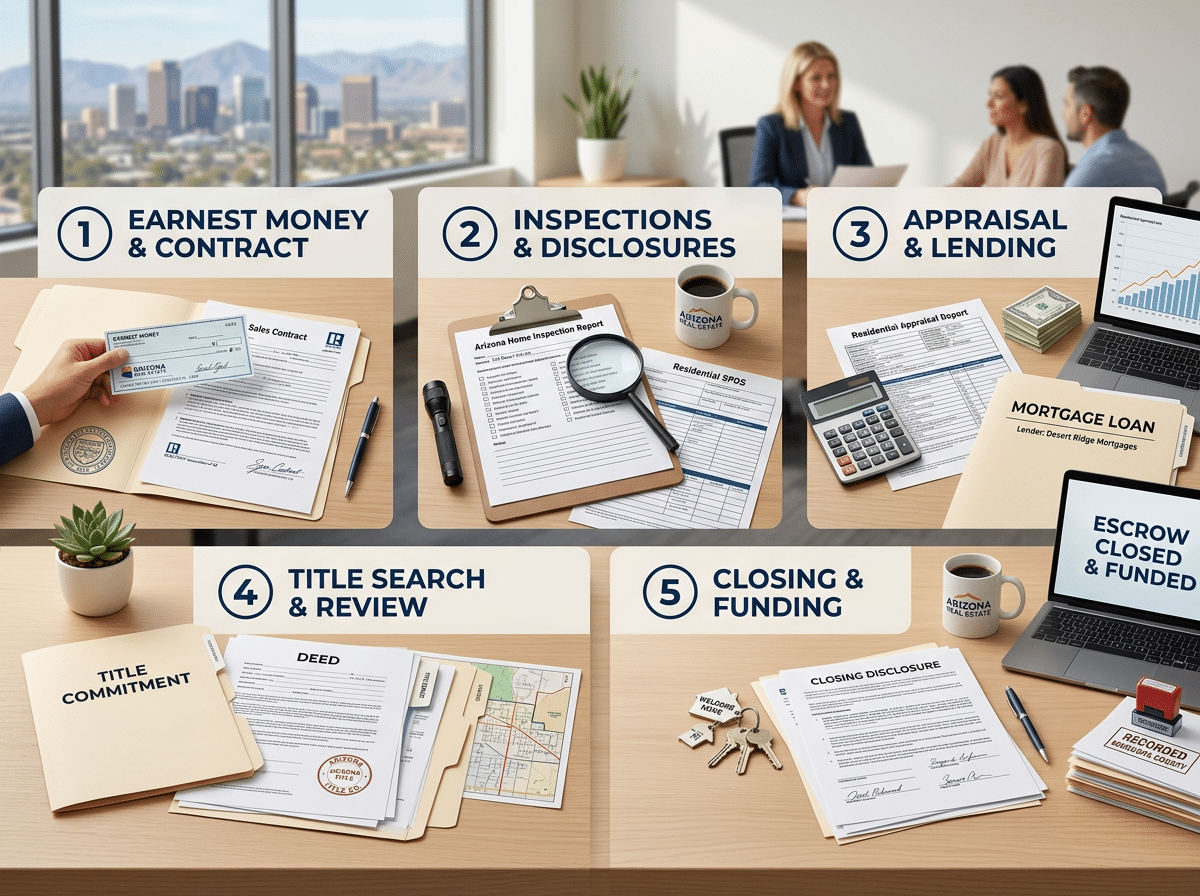

Earnest money is one of the first “real” steps in buying a home—and in earnest money in Arizona situations, it can feel high-stakes because you’re handing over thousands of dollars before you even own the house. The good news: once you understand what earnest money is, where it goes, and what makes it refundable (or not), it becomes a smart tool—not a scary mystery.

Below is a clear, buyer-friendly breakdown of how earnest money works in Arizona, what to watch for, and how to protect your deposit from the moment your offer is accepted until closing day.

What Is Earnest Money?

Earnest money is a deposit you submit after your offer is accepted to show you’re acting in good faith. It tells the seller, “I’m serious, and I’m willing to put money behind this contract.”

In most Arizona transactions, earnest money is:

- Held by a neutral third party (often the escrow/title company)

- Applied to your purchase at closing (it’s typically credited toward your cash to close)

- Governed by the contract timelines (your contingencies and deadlines matter)

Earnest money is not a “fee” you lose automatically. It’s more like a deposit with rules—rules that are spelled out in the purchase contract and tied to your buyer protections (like inspections, appraisal, and loan approval).

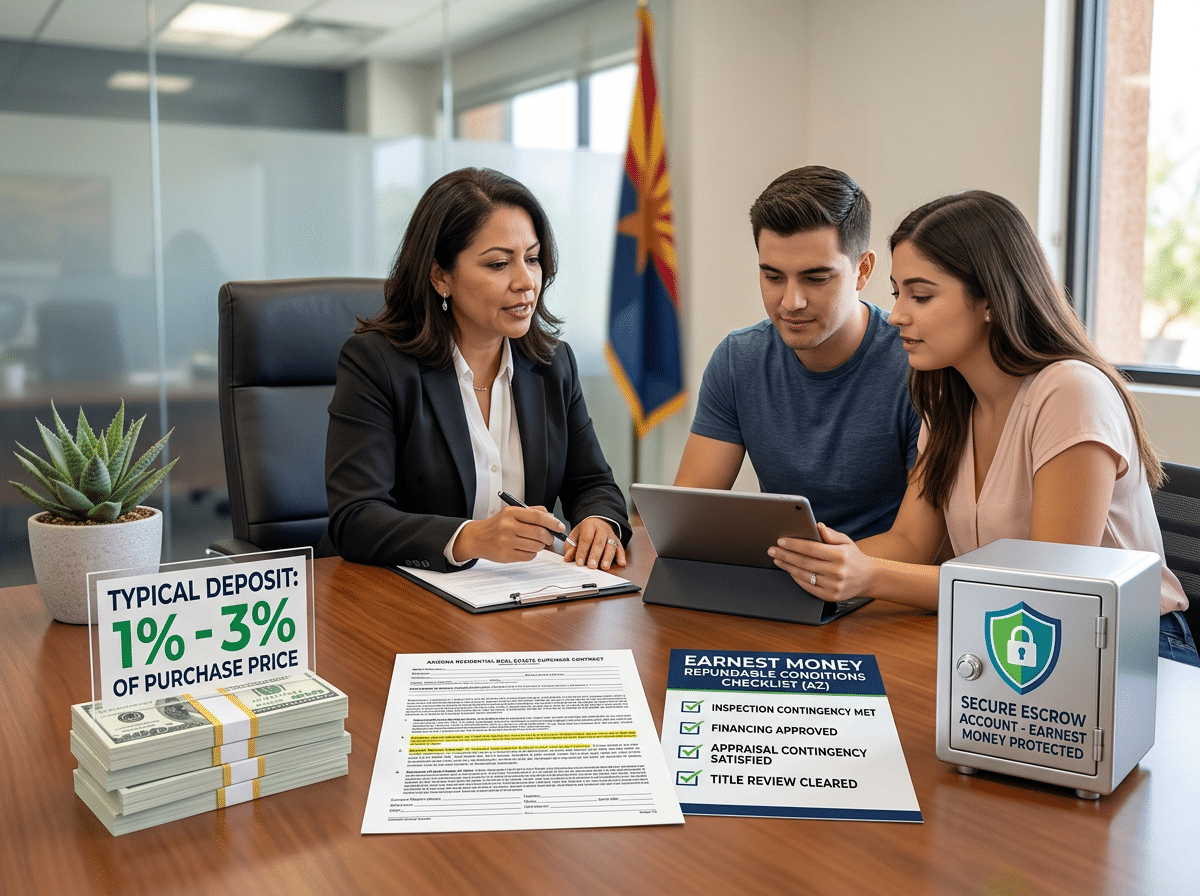

How Much Earnest Money Do Buyers Typically Put Down in Arizona?

There’s no single “standard” earnest money amount statewide—because the right amount depends on price point, market conditions, and how competitive the home is.

That said, you’ll commonly see:

- A flat amount (often a few thousand dollars) for entry-level to mid-range homes

- A percentage-based amount (sometimes around 1% of purchase price) in more competitive situations

In hot pockets of the Valley—like parts of the Phoenix real estate market or certain Scottsdale neighborhoods—sellers may view a stronger earnest money deposit as a sign that a buyer is less likely to walk away.

Bigger deposit = stronger offer?

Sometimes. But it’s not always the smartest move.

A higher earnest money amount can make your offer feel more solid, but it also increases what could be at risk if you miss deadlines or cancel outside your contract protections. The “best” deposit is the one that strengthens your offer while still fitting your comfort level and strategy.

Where Does Earnest Money Go?

Earnest money is typically deposited with the escrow/title company after acceptance (based on the contract’s instructions and timeline). It’s usually held in a trust account and not released to the seller just because escrow opened.

Common ways earnest money is delivered

- Wire transfer

- Cashier’s check

- Personal check (sometimes allowed, depending on the situation)

Safety tip: Always verify wiring instructions by calling a known, trusted phone number (not the number in an email). Wire fraud attempts target real estate transactions because the dollar amounts are large and the timing is urgent. Review the wire fraud advisory for Arizona buyers early so you know the red flags before funds are on the line.

When Is Earnest Money Due?

In Arizona, the contract usually specifies the deadline—often a short window after acceptance. Your Realtor will help you confirm:

- the due date,

- where to send it,

- and how to document that it was received.

This matters because a late deposit can create contract problems (and in some cases, give the seller leverage to issue a notice or potentially cancel, depending on contract terms and how the situation is handled).

Is Earnest Money Refundable in Arizona?

Often, yes—if you cancel within the contract’s contingency periods and follow the contract process.

Earnest money is typically refundable when a buyer cancels properly under protections like:

- Inspection/due diligence period

- Appraisal-related issues (depending on contract terms)

- Loan approval/financing contingency (depending on contract terms)

- Title problems that can’t be resolved

Earnest money becomes more at-risk when:

- a contingency deadline passes, and

- the buyer cancels without a remaining contractual reason, or

- the buyer breaches the contract terms.

The big concept: deadlines control your risk

Most earnest money disputes come down to missed dates, misunderstood contingencies, or incomplete paperwork. That’s why it helps to understand the structure of the purchase contract itself—especially if you’re buying for the first time. The overview of the Arizona Residential Resale Real Estate Purchase Contract is a solid starting point if you want the “why” behind the timelines.

Earnest Money vs. Down Payment: What’s the Difference?

This is one of the most common buyer confusions.

Earnest money:

- happens early (right after acceptance),

- shows commitment,

- is held by escrow,

- is typically credited toward closing costs/cash to close.

Down payment:

- is tied to your mortgage and loan program,

- is paid at closing (as part of your total funds needed to close),

- directly affects your loan amount and sometimes your interest rate/PMI.

In other words: earnest money is not “extra money.” It’s usually part of the funds you were already planning to bring to closing.

What Happens to Earnest Money at Closing?

At closing, earnest money is typically applied as a credit on your settlement statement/closing disclosure. It reduces the amount you need to bring in at the end because you already deposited funds earlier.

Example (simple illustration):

- You deposit $5,000 earnest money

- Your final cash-to-close is $22,000

- That $5,000 is credited, so you bring the remaining difference (after all credits/debits are accounted for)

Your lender and escrow officer will provide the final numbers—always use those final figures rather than guessing based on earlier estimates.

What Could Cause a Buyer to Lose Earnest Money?

No one wants to think about it, but understanding the risk is exactly how you avoid it.

Here are common scenarios that can put earnest money at risk:

Missing your contingency deadlines

If your inspection period ends and you haven’t responded properly, canceling afterward can be more complicated.

Canceling without a contract-protected reason

If you simply “change your mind” after deadlines have passed, the seller may claim the earnest money (depending on contract terms and how the cancellation occurs).

Failing to follow the contract process

In real estate, how you do something matters. Notices, signatures, and timing can be the difference between a clean cancellation and a dispute.

Not being able to perform

If a buyer can’t close because they didn’t secure financing (and they no longer have a financing protection), it can create earnest money risk. This is one reason buyers should get fully pre-approved and keep their lender in the loop throughout escrow.

How to Protect Your Earnest Money (Practical Buyer Tips)

If you remember nothing else, remember this: earnest money is safest when you’re proactive.

Here are simple ways to protect your deposit in Arizona:

1) Schedule inspections immediately

Inspectors can book up—especially during busy seasons. The faster you inspect, the more time you have to negotiate or cancel within your inspection window.

2) Read disclosures early (not the night before the deadline)

Disclosures can reveal HOA restrictions, past repairs, and other details you’ll want to evaluate before your contingency period ends.

3) Stay responsive during escrow

A day or two of delay can matter when deadlines are tight. Quick responses keep your options open.

4) Avoid financial changes mid-escrow

New car loans, big credit card spending, and job changes can create financing issues. Keep your lender updated and avoid major changes until after closing.

5) Treat wiring like a high-security transaction

Again: verify. Use known numbers. Slow down. Fraudsters rely on urgency.

Earnest Money Strategy in Different Arizona Markets

Earnest money isn’t just a checkbox—it’s part of an offer strategy, and strategy changes by location and competition.

- In areas with lots of first-time buyers (certain parts of the East Valley, including Gilbert and nearby suburbs), earnest money can be one of several terms used to show seriousness—alongside timelines and concessions.

- In fast-moving new-build and move-up markets (including communities near Queen Creek), buyers may use earnest money alongside flexible closing dates or shortened inspection windows (only when comfortable) to strengthen an offer.

The right approach depends on the home, the seller’s priorities, and your risk tolerance.

What If There’s a Dispute Over Earnest Money?

Most transactions don’t end up here, but it’s helpful to understand the basics.

If a deal falls apart and the buyer and seller disagree on who should receive the earnest money, escrow typically can’t just “pick a side.” The contract and written instructions determine the process, and the parties may need to sign releases or follow a formal dispute process.

This is where having an experienced agent matters—not to “fight,” but to prevent disputes through clean timelines, proper notices, and solid documentation from the beginning.

FAQs About Earnest Money in Arizona

How much earnest money do I need in Arizona?

It varies by home price and competition. Many buyers use a flat amount (often a few thousand dollars) or a percentage-based deposit, depending on the offer strategy.

Is earnest money always refundable?

Not always. It’s typically refundable if you cancel within your contract contingencies and deadlines, and follow the required process.

Can a seller take my earnest money if I cancel?

Potentially—especially if you cancel after deadlines or without a contract-protected reason. Your Realtor can help you understand your specific risk based on your contract dates.

Is earnest money the same as a down payment?

No. Earnest money is an early deposit held by escrow and usually credited at closing. The down payment is the portion of the purchase price you pay at closing as part of your loan structure.

When do I pay earnest money after my offer is accepted?

Your contract will specify the deadline—often shortly after acceptance. It’s important to deliver it on time and confirm receipt.

Ready to Make a Smart Offer (With the Right Deposit Strategy)?

Earnest money is one of the easiest parts of the offer to misunderstand—but once you know how it works, you can use it confidently to strengthen your purchase without taking unnecessary risk. If you’re preparing to buy, connect with West USA Realty for guidance that fits your budget, timeline, and neighborhood goals. You can also start narrowing your options by browsing Arizona homes for sale and learning the full process inside the Arizona buyer resources hub.